Mohamed Rodani

Physics @ QMUL • Machine Learning, Quant Finance & Scientific Computing

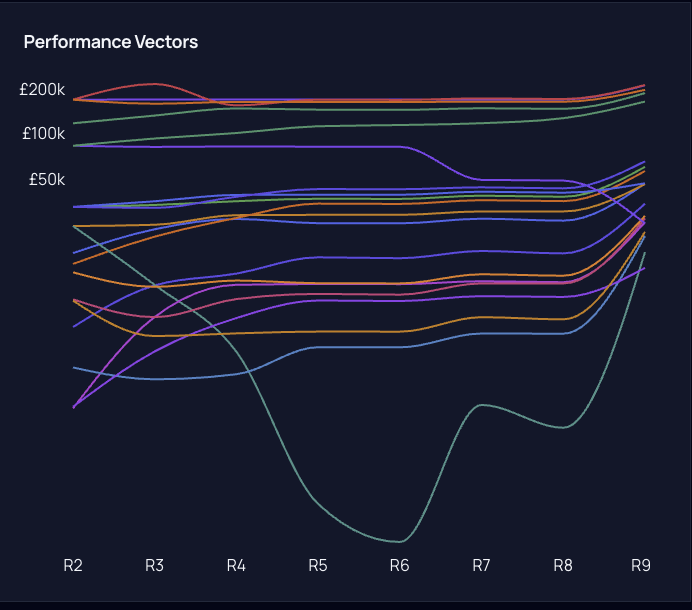

Physics student at QMUL building quantitative finance and ML systems. 2nd out of 93 teams in a live market-making competition. Hackathon winner. Targeting ML engineering roles in quantitative finance.

2nd/93 Market Making

Hackathon Winner

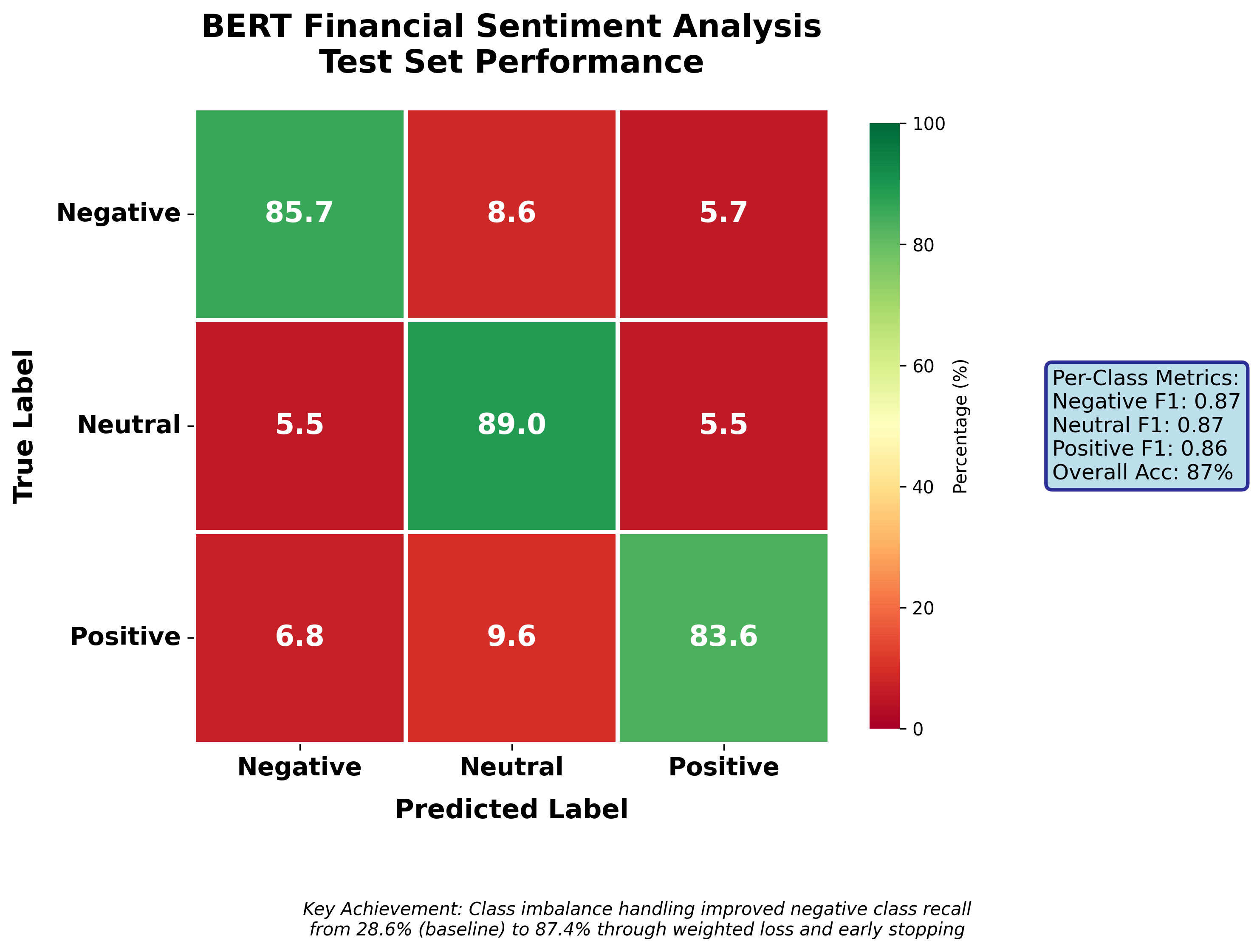

BERT NLP

PyTorch

Python

Quantitative Finance

Quick Facts

Education

Physics @ QMUL

Interests

Currently

Building quant finance projects + applying for spring weeks

Open to

Internships + collaborations